2) Personal Protection Insurance, this was another bolt on scheme that shifted the responsibility to the individual away from government’s responsibility to provide Welfare when unemployed. So via the fear of unemployment, the policy of mortgage interest being covered was now pushed onto the mortgagee, to now be responsible and therefore insure against unemployment, so as to cover the monthly repayments. It later turned out these packages were hard to claim.

Note; if self employed you could not be made redundant, and you could only claim if you were made….redundant!

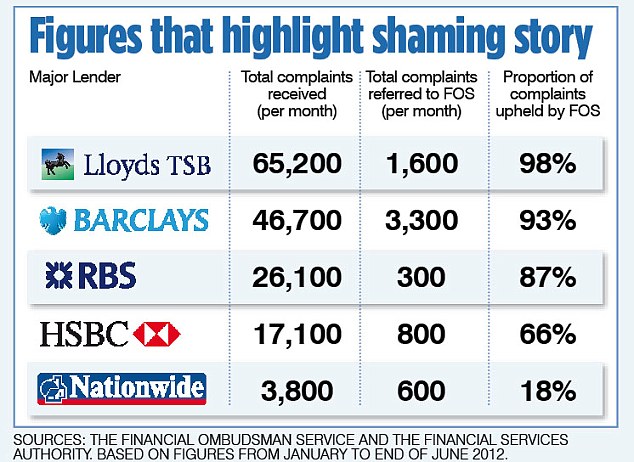

“I personally experienced this as a self employed individual, and paid 5 years of PPI payments for a policy that was not applicable for my self employment, the media eventually exposed this, a change in the law followed, but was too vague to be to enforceable“

The reality was that you were supposed to be able choose and not be forced to take a PPI on any loan or credit card.

Again with my second mortgage I tried to choose not take on a PPI, then at the last moment, when the property was ready for exchange, I was told I could not have the mortgage unless I took this policy, I wrote a letter of complaint, no reply. Thankfully, I kept a copy, 25 years later when PPI claims were costing the banks millions in compensation, I made a claim, it was refused saying I was given an option at the time, 25 years ago my word against theirs in a small Building Society branch with no records. I therefore presented the copy of the letter from 25 years previous to the Ombudsman (a regulatory independent government funded organisation for disputes that banks and building societies had to abide to their decisions as final, based on Law) who agreed with my claim, after a year of wrangling I was compensated, but an average of 8% over the period rather than compounding the amount on annual interest (ie a compromise for the banks). Which ironically is how they earn so much money in the first place for mortgages by compounding annual interest.

So a seemingly a good idea for protection was in fact just another way of extracting money by pushing the responsibility on the borrower and then the lender had now secured their created credit with even less risk and thus they could in turn could lend to less secure mortgagees, which brings us neatly to another opportunity to deregulate and include more risk, whilst making sure any accountability is placed upon the borrower and not the lender, thus no 3.