Original outline comment

(After watching a video by a left-of-centre political commentator, ‘A Different Bias’, I asked him to read my comment, but he probably didn’t. It was a good exercise, nonetheless.)

My comment on the video

Ok, rent controls. This has been my area of research for the past 9 years.

1) Any rent freeze, as in WW1 and WW2, HAS to be backdated for the obvious reason of a mad rush by landlords to pre-empt.

2) The trap of a rent freeze is a doubling of rent when it ends. The Lloyd George government promised to end the freeze 6 months after the cessation of war. The issue was the fear that it would really piss off a lot of battle-hardened men and women. (Remember, at least 80% were renting from the private rental sector, PRS.) So they introduced a form of rent control that quickly became very complicated and messy.

3) Solution: Keep it SIMPLE and UNIVERSAL. All PRS (as in my own rent-controlled shared ownership) max per annum at CPI (not RPI or RPI +1-2%). All properties based on local value to be assessed at the beginning of a contract at 3% of value per annum, reassessed every 5 years to account for falling property values, which will fall. As the PRS will now refuse to build ‘build-to-rent’ property, the government will be forced, as in the 1919 housing act, to have an ongoing scheme of building social housing, NOT via housing associations until they are also reformed concerning the present scams of ground rent, unregulated buildings insurance and ‘service charges’.

4) Max repayment over 25 years for repayment, no more commercial/stock market-linked bank lending, only highly regulated mutual building societies, always at least 0.25% below base rates.

5) Government to take back interest rate control from the central bank, whose remit has no nuance and remains a blunt instrument that hammers borrowers over those who are already wealthy and then benefit via higher interest rates.

6) Make mortgage money scarce, not land, by controlling annual lending volumes to curb land inflation (think of a gatekeeper). The money cannot inflate (scarcity) because it’s controlled by the creator (i.e., the government by decree, fiat). This happened from the 1950s-70s ( Stop/go policy) and often meant waiting an extra year, but it kept housing affordable, as speculators could not profit from the highly regulated control over the naturally monopolistic thing called Land, one of the three pillars of economics, namely Capital, Labour and Land, via Adam Smith and all the classical economists, also Marx, Keynes and Galbraith. Hayek and his crew decided under neoliberal theory that land (that cannot be made) is now a product and therefore a ‘capital asset, it’s clearly not, ‘it’s the mother of all monopolies’ (ref Winston Churchill 1909).

7) Capital and Labour at the same progressive rates of taxation. Very high inheritance tax on properties (progressive): £3 million and above, i.e., 70-90%. meaning each generation has to make its own way, but now possible, as land values (as proven from 1915-1970 and in the Nordic countries, Ref. Viking Economics by George Lakey) will fall as housing is no longer a commodity. Note that this worked through the housing shortages of the 1950s.

8) The PRS will abandon and look for easier profits, and will often sell to their sitting tenants. This will happen over 30 years, due to the illiquid nature of housing.

9) For this to work, it is really important that there are at least 5 different but interconnected forms of legislation; otherwise, it will fail and then be abandoned for another 40 years. (Rent Control 1915-1988).

Any trolls out there? This is a massive subject, and, like Beveridge’s report (1942), it will require a 10k-word-plus document to address the known consequences. The unknowns will have to be tackled, and the unknown, unknowns, well, I’ll leave them to the next generation.

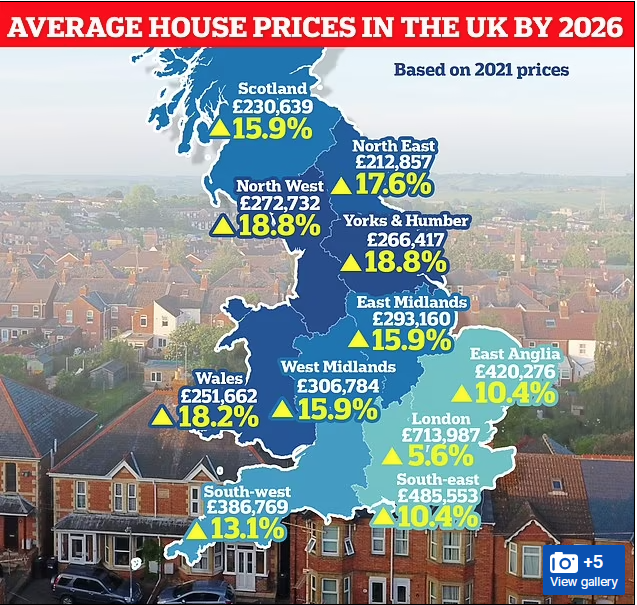

Just a note on affordability. We are paying, on average, £550,000 too much for houses in the Southeast compared with the 1950s (inflation-adjusted) due to land values (the speculative part of a house). Land now accounts for 70% instead of 10% (the build cost has broadly kept pace with inflation). An 86m2 semi should be £200K, not £750K, in 2026.