The Housing Act of 1988 deregulated new lettings to encourage the PRS to return, 44 years later the potential for 1910 rent strikes of pre The Rent Control Act of 1914 look like they may return.

Sitting in the library, grinding my way through various papers and journals on Rent Control (RC), I started to read a report from the much admired Joseph Rowntree Foundation (JRF) published in 1992 with various academic, housing pressure groups, practitioners and financiers together with advisors to politicians from different parties all contributing to the discussion. So far so good, but…..

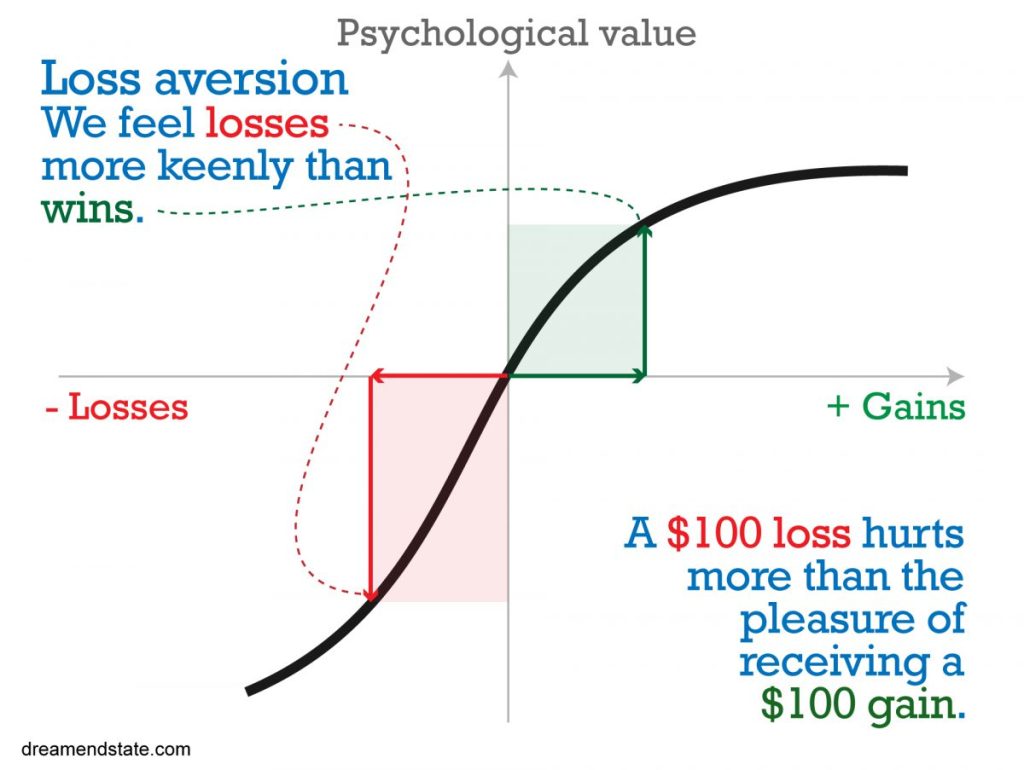

Two issues of cognitive bias became increasingly apparent, both of which we all suffer from as emotional beings, so I’m not specifically criticising the authors of the report, but taking the more cautious route of an anthropologists like, the sadly departed David Graeber and also the political economist Thomas Piketty. Graeber in his book (and the secret is in the title) Debt; The First 5000 years and Piketty to a lesser extent focussed on the past 200 years in his highly acclaimed and fascinating book Capital of the 21st Century.

“Recency bias is a cognitive bias that favors recent events over historic ones“

The first bias was the effect of just looking to the lived and experienced recent past (recency bias) and making a judgment that a correlation of rent controls of the recent past have meant that the PRS has reduced due to not enough yield being available from old RC properties, that is a fair judgment, but does that mean that to get more rented properties available for the small sector (at the time of the report) of transient renters, namely young people on their way to purchase and temporary work force ( in fact a red herring) moving around the country, you just simply reverse the model?

So with that logic, if rent control causes PRS shortages then abandon rent control and supplement the PRS and a ‘fair’ rental market will return with the benefit of landlords now also getting a ‘fair return’.

“What could possibly go wrong’?

The issue with this decision is that now in 2022 we are seeing the true consequences of this reversal, rather than market rates settling to a ‘fair rent’ level they are driving people into cohabitation and single room conversions with shared bathrooms as incomes have stagnated (not so much trickle down, but rather, trickle up), but rents increase as scarcity within the ‘free market’ predicts.

Whereas if they had taken the time and effort to look back to pre 1914 Rent Act they would’ve seen the issues of free market rents gradually consuming and therefore monopolising a sector that even Winston Churchill in 1909 fumed and rallied against to the greed and slothfulness of the rentier class.